U.S. Oil Under International Pressure

Inside the week’s crude draws, product builds, and pricing signals amid rising global risk

Oil in the Crossfire — Geopolitics Collide with U.S. Trends

The Israel–Iran conflict has ignited fresh volatility in global oil markets just as U.S.–China trade negotiations re-enter the spotlight. With geopolitical risk rising and crude prices reacting, U.S. refiners are pushing throughput to multi-year highs—yet product demand isn’t keeping pace. For investors watching the U.S. energy sector, the latest EIA data offers critical insight into whether current trends signal strength, oversupply, or an inflection point in the shale cycle.

📩 Want deeper insights like this every week? Subscribe to PetroSymposium for high-impact analysis on crude markets, shale trends, and energy investing—built for investors, analysts, and energy professionals.

👉 Subscribe now for full access.

Refiners on Full Throttle: Seasonal Demand Kicks In

U.S. refinery inputs averaged 17.2 million barrels per day for the week ending June 6, 2025, up 228,000 bpd from the prior week — the highest since early 2020. Utilization rates rose to 94.3%, the strongest in nearly five years.

Gasoline production increased to 9.7 million bpd, matching seasonal norms. Meanwhile, distillate production fell 97,000 bpd to 4.9 million bpd, reflecting tight diesel and jet fuel supplies.

Despite higher refinery runs, crude inventories fell last week but gasoline and distillate stocks rose, suggesting weaker end-user demand. The key will be whether refiners reduce runs to manage product oversupply or maintain output hoping for demand to catch up.

Import Flows Slow: Structural Shifts Underway

U.S. crude imports averaged 6.2 million bpd last week, down 170,000 bpd from the prior week and 13.3% below last year’s four-week average.

This decline may reflect geopolitical shifts, OPEC+ production changes, and weakening domestic demand. Gasoline imports remain high at 914,000 bpd, likely driven by local supply needs but also hinting at overestimated consumption.

Overall, the U.S. is balancing geopolitics, refining cycles, and softer demand with more cautious crude buying.

Inventory Tug-of-War: Crude Draws, Product Builds

Crude inventories fell 3.6 million barrels to 432.4 million, 8% below the five-year average. Yet, gasoline stocks rose 1.5 million barrels and distillates by 1.2 million, with propane inventories notably up 4 million barrels heading into export season.

Total petroleum stocks increased 6.2 million barrels, reinforcing the ongoing divergence: crude draws upstream versus product builds downstream.

Demand Snapshot: Mixed Signals

Total product supplied over the last four weeks averaged 19.9 million bpd, up 0.5% year-over-year. Gasoline supply dropped 2.5%, distillates fell 5.9%, while jet fuel rose 1.3%.

This mix points to steady overall demand but weakness in key sectors, keeping downstream pressure on refining margins.

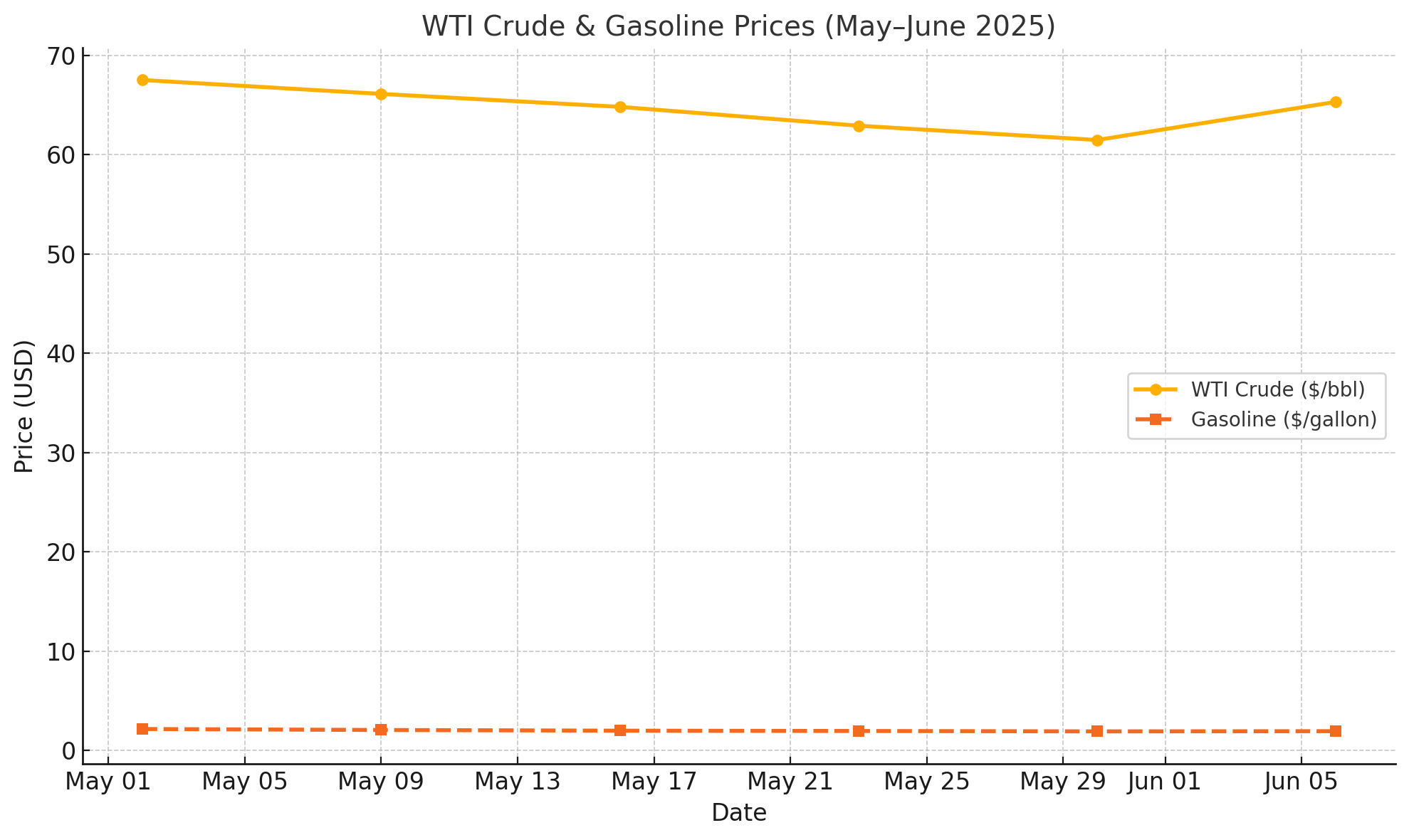

Price Movements: WTI Up, Still Below Last Year

On June 6, WTI crude closed at $65.30 per barrel, up $3.84 from last week but $11.23 below last year.

Gasoline prices edged up slightly to $1.93/gallon but remain $0.45 below last year’s level. Heating oil prices reflect distillate market tightness despite some inventory gains.

Recent crude gains are supported by geopolitical tensions, OPEC+ supply management, and seasonal refinery activity.

Looking Ahead: Crude Prices Likely to Rise

Crude prices for Brent and WTI should climb in coming weeks due to:

Progress in U.S.-China trade deals boosting demand

Seasonal demand increases during summer

Elevated geopolitical tensions in the Middle East

These factors support higher crude prices despite mixed demand signals downstream.

Retail Fuel Prices: Gasoline Falls, Diesel Holds

As of June 9, the national average gasoline price fell slightly to $3.108/gallon, down $0.019 week-over-week and $0.32 below last year.

Diesel prices rose modestly to $3.471/gallon but remain $0.19 lower year-over-year, supported by tighter distillate fundamentals.

Conclusion: Balancing Supply, Demand, and Risk

U.S. crude inventories are tightening while refined product stocks rise, creating upstream bullishness but downstream caution.

Prices may increase amid Middle East tensions and trade progress, but refinery runs must be watched closely. If production outpaces demand, inventories could build, pressuring future margins.

The key risk lies in how quickly refiners adjust capacity if demand shifts. In this volatile market, staying alert to geopolitical and operational trends is critical.

💡 Enjoyed this breakdown?

Unlock exclusive energy forecasts, valuation models, and global oil insights by upgrading to PetroSymposium Premium.🔓 Go Premium — and stay ahead of the next crude cycle.