The Canadian Oil Giant That Could Make You Rich?: Suncor DCF Valuation Analysis

A deep dive into Suncor’s cash flow power, upside potential, and capital return profile—why this Canadian energy stock deserves a second look.

Unlocking Suncor’s True Value — Why It’s a Buy

After reviewing Suncor’s strong Q1 operational momentum in Part 1, we now turn to valuation. Despite ongoing macroeconomic headwinds, Suncor’s robust free cash flow generation and disciplined capital return strategy create a compelling long-term investment opportunity. Our discounted cash flow (DCF) model supports a Buy recommendation with meaningful upside potential.

🔍 Want the full DCF model behind this valuation?

Gain access to the downloadable Excel forecast, scenario analysis, and future company breakdowns.

👉 Join PetroSymposium Premium to elevate your energy investing edge.

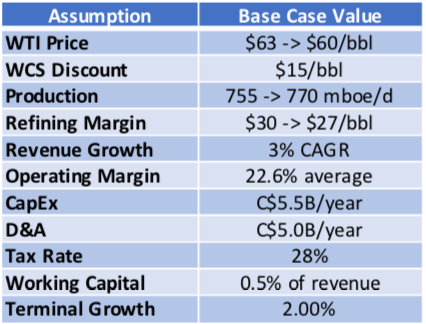

Key Forecast Assumptions

Our financial forecast incorporates a base-case outlook aligned with market realities and company guidance, factoring in commodity prices, cost structure, and capital expenditure plans.

Keep reading with a 7-day free trial

Subscribe to Petro Symposium: The New Generation of Wealth to keep reading this post and get 7 days of free access to the full post archives.